An introduction to leveraged buyouts

updated on 04 June 2019

Question

How do leveraged buyouts combine private equity and debt finance to provide an attractive way to finance transactions?Answer

Private equity means equity financing of unlisted companies at various stages of that business’s lifecycle, from start-up, to expansion, to management buyouts, to buy-ins of established businesses. The key features of private equity are: (i) acquisition of equity in unquoted companies; (ii) medium to long-term investments; and (iii) target companies with growth potential.

Private equity is invested by a private equity fund (a sponsor) in exchange for a stake in a company (a target). The sponsor’s goal as a shareholder is to increase the value of the target in order to make a profitable exit. A profitable exit can be achieved in two main ways: (i) paying down the target’s debt so equity becomes relatively more valuable; and (ii) operational improvements to the target’s business (ie, cutting costs, improving productivity and increasing profits).

The Sponsor will look to achieve operational improvements and drive financial returns by aligning the financial interests of the target’s management with those of the sponsor. On acquisition of the target, management may also own shares in it so strong performance is rewarded not by increases in salary/bonus, but through an increase in the value of the target and according increases in the value of the sponsor and management’s investments.

What is a leveraged buyout?

A leveraged buyout (LBO) is the acquisition by a sponsor of a target using a combination of equity finance (in the form of share capital and subordinated loan capital) provided by a private equity fund and a substantial amount of debt finance provided by a bank or other financial institutions, secured against the target and the other group companies’ assets.

Benefit of the LBO structure

The benefits of the use of debt in combination with equity are:

- the ability to financially engineer more attractive returns on equity;

- the sponsor is able to make number of acquisitions without committing too much capital;

- greater stability in source of funds compared to private equity; and

- debt is effectively cheaper than equity.

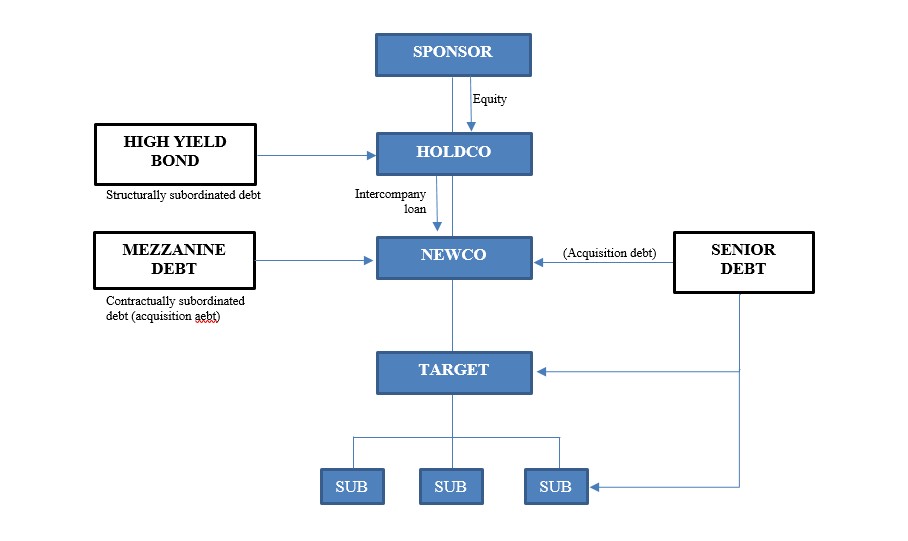

Summary of a simple transaction structure for leveraged finance

Typically, there will be two special purpose vehicles (SPV) established by the sponsor – Holdco and Newco. Holdco will act as the investment vehicle which the sponsor will use to inject equity. Holdco will subscribe to the equity of Newco. Newco will act as borrower and acquiring vehicle for the target.

Types of acquisition finance

Senior debt

Senior debt provided by senior lenders is the principal source of acquisition finance. It typically takes the form of a floating rate medium-term loan for primarily funding the acquisition and for other financing requirements specified in the facility agreement. The senior debt would usually also have revolving credit facility, which is a line of credit that can be borrowed, repaid and re-borrowed at any time prior to the maturity date of the term loan – like an overdraft facility. The senior debt will rank higher in the capital structure than any other debt, so it must be repaid in full before any other source of debt. This relationship between the creditors will be documented in an intercreditor agreement.

Mezzanine debt

Mezzanine loans are bank loans secured on the same assets of the senior debt but are contractually subordinated under the intercreditor agreement. Mezzanine loans typically have no amortisation and a bullet repayment is made upon maturity of the loan, which is typically six to 12 months after the maturity of the last maturing tranche of the senior debt. Mezzanine loans have a higher interest rate than the senior debt as they carry higher inherent risks. The interest rate is typically a combination of cash or payment in kind (PIK).

High-yield debt

High-yield debt takes the form of a bond (also called notes) typically issued by Holdco and usually flows to Newco via an intragroup loan from Holdco to Newco. These notes are rated ‘sub-investment grade’ by rating agencies. To be commercially viable, high-yield notes rely on very strong cashflow streams from the target business. The size of the issue must also be sufficient for there to be a market for the bonds. High-yield note is typically an alternative form of junior debt to mezzanine debt and is used in large transactions.

Note: there are other types of acquisition finance, such as unitranche, senior lien debt and PIK note debt.

Summary of the parties involved in a leveraged finance transaction

Sponsor

This is the financial sponsor of the deal and the real economic buyer in a buyout.

Holdco

Holdco will act as the investment vehicle which the sponsor will use to inject equity. Holdco will subscribe to the equity of Newco.

Newco

The buyer of the target company. Newco will be an SPV, which has not previously traded and is therefore bankruptcy-remote.

Senior lenders

The senior lenders will likely be providing the majority of the acquisition finance for the buyout under the senior facilities agreement. The senior lenders will consist of banks and institutional lenders. In larger transactions, the senior facilities will commonly be syndicated after completion of the acquisition. It is common for some of the lenders to act as co-arrangers and underwrite the acquisition facilities before syndicating more widely after completion.

Mezzanine lenders

Mezzanine lenders tend to consist of mezzanine funds, together with hedge funds, leveraged loan funds and other institutional lenders. As with senior debt, it is common for the mezzanine facilities to be arranged and underwritten by a select few funders, who will syndicate more widely after the acquisition.

High-yield bondholders

The high-yield bondholders will comprise of institutional investors that are experienced and active in the high-yield markets. The timetable for a successful issue of high-yield bonds is usually unpredictable, therefore the sponsor tends not to align the timetable of issue with the completion of the acquisition. A bridging loan is often used to fill the funding gap, which is subsequently refinanced with the proceeds of the bond issue. The arrangers of the high-yield bond, generally known as managers, will often be one of the mandated lead arrangers under the senior facilities and may also underwrite the bridging loan. The manager will also negotiate the terms of the high-yield bond on behalf of the bondholders.

Target

Newco will acquire the shares of the target and thus the target and all its subsidiaries will come under indirect control of the sponsor. As conditions subsequent to the acquisition, often the target’s subsidiaries will accede to the principal finance documents as obligors and they will grant share and asset security to the security trustee (on behalf of the lenders).

Seller

The role of the seller is often distant from the acquisition finance. The seller’s main concern is the sale of the target and is less concerned with the source of the funds used in to acquire the target.

Dimeji Ademiju and Marwan Al Rasheed are, respectively, an associate and trainee associate at Weil, Gotshal & Manges.